An interesting data point emerged this week. On Tuesday evening, the Department of Education, after months of operational silence on the matter, sent a wave of emails to a specific cohort of student loan borrowers, an event captured by Mass Student Loan Forgiveness Emails Sent To Borrowers As IBR Pause Appears To Lift. The message was unambiguous: after 20 or 25 years of payments, their remaining debt under the Income-Based Repayment (IBR) plan was finally eligible for discharge.

Online forums, a useful if imperfect source of anecdotal sentiment, lit up immediately. Borrowers on Reddit posted screenshots of the "golden email," some expressing disbelief after years of waiting. One user with a balance over $200,000 and a payment count of 322 (well past the 300-payment threshold) described sitting in tears. This wasn't a policy announcement broadcast from a podium; it was a quiet, direct-to-consumer data transmission that signaled a significant, if narrowly defined, shift.

The immediate question is not what happened, but why it happened now. The resumption of this specific `student loan forgiveness program` was not accompanied by any formal press release or statement from the department. The action itself is the only signal we have. And when an administrative body acts silently and suddenly, the catalyst is rarely spontaneous benevolence. It’s usually external pressure.

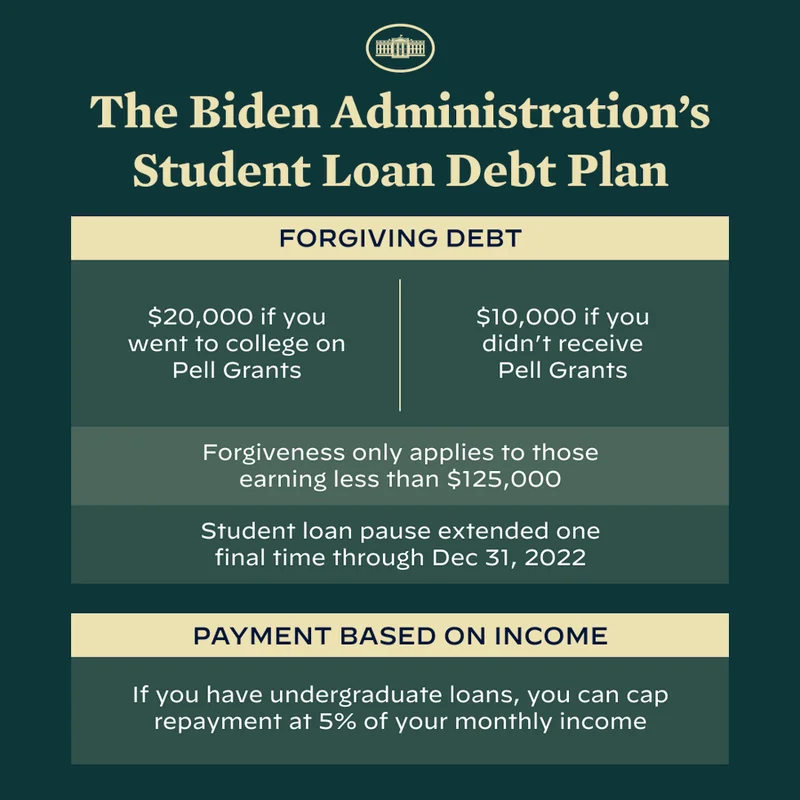

To understand the context, we have to look at the sequence of events. The IBR plan, established by Congress in 2007, was the last man standing in the world of `federal student loan forgiveness`. While other income-driven plans like SAVE, PAYE, and ICR have been frozen by litigation targeting the Biden administration's broader relief efforts, IBR’s congressional mandate gave it a separate legal foundation. It was, for a time, the only game in town.

Then, in July, even that stopped. The department quietly paused IBR discharges, citing a need to update its systems. For borrowers who had spent a quarter-century paying into the system and were finally crossing the finish line, the goalposts suddenly vanished.

And this is the part of the report that I find genuinely puzzling from a strategic standpoint. The department created a new liability for itself. By halting a congressionally authorized program, they opened the door to legal action. That’s exactly what happened. The American Federation of Teachers (AFT), already in a legal battle over other stalled forgiveness programs, amended its lawsuit last month to include the "unwarranted and unlawful" delay in IBR processing.

The correlation here is too strong to ignore. Lawsuit amended in September, forgiveness emails sent in early October. Following the news that the Trump administration resumes student loan forgiveness, Randi Weingarten, the AFT president, didn't mince words, stating, "We stood up to them in court and demanded that they follow the law. Right away, the U.S. Department of Education changed its tune." This isn't a policy evolution; it appears to be a forced correction in the face of a credible legal threat. The department hasn't changed its mind; it may simply have been compelled to change its behavior.

This action is like a single gear in a complex, seized-up machine being forced to turn by an external lever—the lawsuit. While that one gear moves, the rest of the mechanism remains frozen. The underlying legal challenges that have halted the SAVE, PAYE, and ICR plans haven't gone away. The `Trump student loan forgiveness` landscape, as it stands, is now a fractured system where relief depends entirely on which acronym your loan falls under. Does this tactical retreat on IBR signal a broader strategy, or is it merely an attempt to neutralize a single, potent legal attack?

The resumption of IBR discharges creates a clear, two-tiered system for borrowers. If you are one of the roughly 2 million people enrolled in the IBR plan—though to be more exact, only a fraction of those have made enough payments to qualify—you now have a path forward. If you are in any of the other income-driven plans, you remain in limbo, watching as a legal battle over the SAVE plan holds your financial future hostage.

This bifurcation introduces significant new uncertainties. The most pressing is a fiscal cliff that has nothing to do with government shutdowns. A provision in the 2021 American Rescue Plan makes `student loan forgiveness taxable` status temporary. That protection expires on December 31, 2025. For the borrowers receiving these emails, the clock is now ticking loudly. The department’s notice gives them until October 21 to opt out, after which processing could take "two weeks" for most, but "longer for some."

How much longer? And what happens if processing delays—compounded by a potential government shutdown that could furlough nearly 90% of department staff—push a borrower’s discharge date into 2026? A life-changing debt cancellation could instantly become a massive, unexpected tax liability. This isn't just an administrative delay; it's a variable with five- or six-figure consequences for families. We have no clear data on the department's processing capacity or how they will prioritize these discharges against the looming tax deadline.

The core issue remains unresolved. The AFT lawsuit isn’t just about IBR; it’s also about the tens of thousands of public servants trying to "buy back" time spent in forbearance to qualify for `public service student loan forgiveness` (PSLF) and the borrowers stuck in the other stalled plans. Persis Yu, an attorney for the AFT, noted that restarting IBR forgiveness doesn't resolve the problem for those in PAYE or ICR. The `student loan forgiveness lawsuit` will almost certainly continue, because the fundamental discrepancy in how borrowers are being treated based on their repayment plan's acronym has now been codified by the department's own actions.

My analysis of this situation is that we are not witnessing a change in policy, but a tactical legal maneuver. The Department of Education was facing a direct and compelling lawsuit over its failure to execute a program explicitly authorized by Congress. The path of least resistance was to comply on that single front, thereby weakening the AFT's immediate legal argument. This move isolates the IBR plan from the more contentious, administration-created programs like SAVE, leaving them to be fought over in court. It’s a clean, logical action if your goal is to contain a legal problem, not to provide widespread relief. The borrowers who received emails this week are simply the beneficiaries of a targeted legal strike. For everyone else, the freeze continues.